Raising a child with autism requires careful financial planning to manage both immediate needs and long-term care. Two key tools often used are emergency funds and special needs trusts (SNTs). Here’s a quick breakdown:

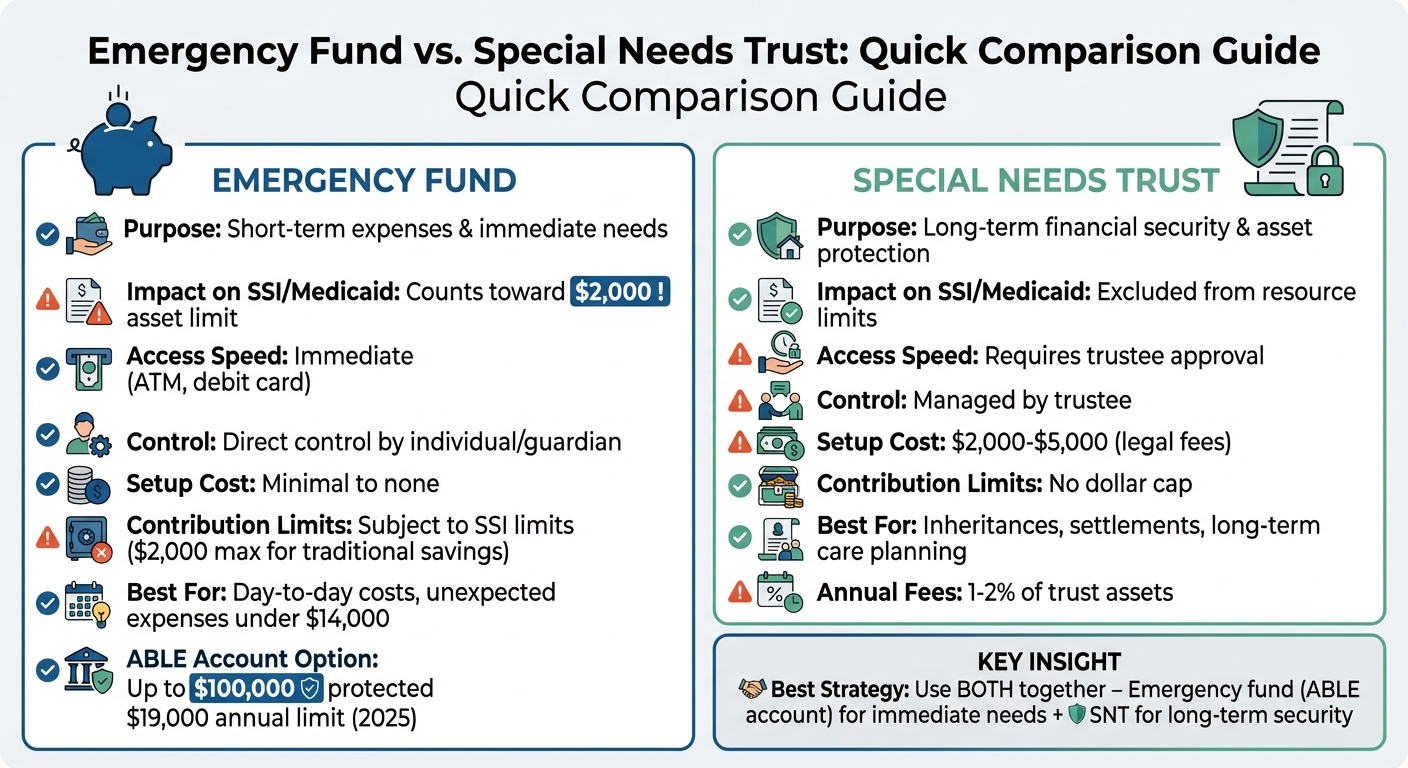

- Emergency Fund: A short-term savings reserve for unexpected costs like therapy, medical bills, or equipment. Accessible immediately, but funds can impact eligibility for government benefits like SSI if they exceed $2,000.

- Special Needs Trust (SNT): A long-term legal arrangement that protects assets while preserving eligibility for SSI and Medicaid. Managed by a trustee, it covers supplemental needs without affecting benefits.

Quick Comparison:

| Factor | Emergency Fund | Special Needs Trust (SNT) |

|---|---|---|

| Purpose | Short-term expenses | Long-term financial security |

| Impact on SSI/Medicaid | Counts toward $2,000 asset limit | Excluded from resource limits |

| Access | Immediate | Requires trustee approval |

| Setup Cost | Minimal | Higher; legal fees required |

| Contribution Limits | None, but subject to SSI limits | No dollar cap |

How to Use Them Together: Use an emergency fund (often in an ABLE account) for day-to-day costs, and an SNT for larger inheritances or long-term care. Together, they balance short-term flexibility with long-term stability.

Emergency Fund vs Special Needs Trust Comparison Chart

Special Needs Trust Explained: Protect Your Child’s Benefits

sbb-itb-d549f5b

What Is an Emergency Fund?

An emergency fund is a savings reserve you can tap into quickly when unexpected expenses arise. For families supporting autistic children, this fund becomes even more critical, covering costs like sudden therapy interruptions, urgent medical bills, or replacing essential equipment.

The standout feature of an emergency fund is accessibility. Unlike long-term financial tools like special needs trusts, you have direct control over these funds, allowing immediate access when emergencies strike. This accessibility is what makes it so essential.

Purpose and Benefits

The primary role of an emergency fund is to handle unexpected financial needs without risking your child’s benefits eligibility. Whether it’s paying for a surprise medical expense, fixing or replacing assistive devices, or covering gaps in therapy services, this fund ensures you’re prepared.

For families with autistic children, an ABLE account is often the best structure for an emergency fund. Unlike traditional savings accounts, which can impact eligibility for Supplemental Security Income (SSI) if balances exceed $2,000, ABLE accounts allow you to save up to $100,000 without affecting SSI or Medicaid benefits.

ABLE accounts are incredibly flexible. Funds can be used for qualified disability expenses (QDEs), which include health care, housing, transportation, assistive technology, and even basic living costs like food. Many ABLE accounts also come with debit cards, making it easy to pay for these expenses directly.

Additionally, ABLE accounts offer tax advantages. Any growth in the account and withdrawals used for qualified expenses are entirely tax-free, adding another layer of financial relief.

Having an emergency fund, especially in an ABLE account, gives you peace of mind and financial stability in the face of unexpected challenges.

How to Build an Emergency Fund

Building an emergency fund requires planning and consistency. A good rule of thumb is to save enough to cover 3–6 months of living expenses. For families managing autism-related costs, this financial cushion provides critical breathing room during emergencies.

If your child qualifies for an ABLE account, consider starting there. Opening an ABLE account is straightforward – you can typically do it online through your state’s ABLE program website. Once the account is set up, make regular contributions while staying within the annual limit, which will be $19,000 for 2025.

Keep an eye on your ABLE account balance. While most states allow balances of $300,000 or more, keeping the balance at or below $100,000 ensures that your child’s SSI cash benefits aren’t affected. Balances above $100,000 are counted as a resource and may temporarily suspend benefits.

What Is a Special Needs Trust?

A special needs trust (SNT) is a legal tool designed to hold assets for a person with disabilities without jeopardizing their eligibility for benefits like SSI and Medicaid. These programs typically have a $2,000 resource limit, but funds in an SNT don’t count toward that cap. Unlike a standard savings account or emergency fund that you manage directly, an SNT is overseen by a trustee. This could be a trusted individual or a professional entity responsible for making spending decisions that benefit your child.

The trust is intended to cover quality-of-life expenses that government benefits don’t address. This includes things like specialized therapies, adaptive equipment, educational programs, travel, and other items or services that improve your child’s day-to-day life. Importantly, the trustee pays service providers directly rather than giving money to the beneficiary. This ensures your child remains eligible for crucial benefits. Choosing the right type of SNT is a key decision for your family’s specific needs.

SNTs also provide long-term financial protection by shielding assets from creditors and lawsuits. There’s no cap on how much money an SNT can hold, making it a smart choice for managing larger inheritances, life insurance payouts, or other significant financial gifts.

Types of Special Needs Trusts

There are three main types of SNTs, each serving different scenarios.

- First-party SNT: This type, also known as a self-settled trust, is funded using the beneficiary’s own money. Common sources include personal injury settlements, direct inheritances, or back payments from benefits. However, it must be created before the beneficiary turns 65. Additionally, when the beneficiary passes away, any remaining funds must reimburse the state for Medicaid expenses paid on their behalf – a rule called the Medicaid payback provision.

- Third-party SNT: This trust is funded with assets from someone other than the beneficiary, such as parents, grandparents, or other relatives. Unlike a first-party SNT, it has no age restrictions and doesn’t require Medicaid payback. Any leftover funds can be passed to other heirs after the beneficiary’s death.

- Pooled SNT: Managed by nonprofit organizations, pooled trusts combine resources from multiple families for investment purposes. Each beneficiary has their own sub-account, but administrative costs are shared. These trusts are often more affordable to set up, with fees ranging from $0 to $1,500 compared to $2,000 to $5,000 or more for individual trusts. Pooled SNTs are a practical choice for families with smaller amounts of money to manage.

Key Features and Benefits

One of the standout features of an SNT is its ability to preserve eligibility for SSI and Medicaid, no matter how much money is in the trust. While ABLE accounts protect up to $100,000 without affecting SSI eligibility, SNTs have no such limit.

The trustee plays a crucial role, deciding how and when to use trust funds while keeping the beneficiary’s best interests and benefit eligibility in mind. Payments are made directly to service providers for things like therapy, equipment, or travel, rather than giving cash to the beneficiary.

A recent change in SSI rules, effective September 2024, allows trustees to cover food expenses without reducing SSI benefits. This update means groceries can now be included in the trust’s spending without penalties.

SNTs often work well alongside ABLE accounts. Families frequently use ABLE accounts for everyday expenses, while SNTs handle larger, long-term needs such as home modifications, vehicles, or ongoing specialized care. This combination offers flexibility and security for managing both immediate and future financial needs.

Key Differences Between Emergency Funds and Special Needs Trusts

Comparison Table

| Factor | Emergency Fund | Special Needs Trust (SNT) |

|---|---|---|

| Primary Purpose | Immediate liquidity for unexpected expenses | Long-term asset protection and benefit preservation |

| Impact on SSI/Medicaid | Counts toward the $2,000 resource limit; can disqualify benefits | Assets excluded; no impact on eligibility if managed correctly |

| Access Speed | Instant (ATM, debit card, transfer) | Slower; requires trustee approval |

| Control | Managed by the individual or guardian | Managed by a trustee with fiduciary duties |

| Contribution Limits | No legal limit (though subject to benefit resource caps) | No dollar cap on contributions or total balance |

| Setup Cost | None to minimal | High; typically requires an attorney and considerable fees |

| Permitted Expenses | Can be used for any expense | Limited to supplemental needs; using funds for food or shelter can affect SSI |

| Estate Planning | Assets pass via will or probate; no Medicaid payback | Third-party SNTs can pass to heirs; first-party SNTs require Medicaid payback |

Analysis of Differences

The table highlights the most important contrasts between emergency funds and Special Needs Trusts (SNTs), and understanding these distinctions can help determine the right financial tool for specific needs.

One of the biggest differences lies in how these assets impact benefit eligibility. An emergency fund counts toward the $2,000 resource limit for Supplemental Security Income (SSI) and Medicaid, which could disqualify the individual from receiving benefits if exceeded. On the other hand, a properly structured SNT ensures that assets are excluded from this resource limit, preserving eligibility.

Accessibility and control are also worlds apart. Emergency funds are immediately available for use, whether through an ATM withdrawal, debit card, or bank transfer. In contrast, SNTs operate under stricter rules. Beneficiaries cannot access funds directly; instead, a trustee must approve expenses and make payments directly to service providers. This ensures compliance with benefit regulations but can slow down the process of accessing funds.

The cost of setting up these tools is another key factor. Emergency funds are essentially free to establish and maintain, while SNTs require specialized legal assistance. Attorney fees and ongoing administrative costs make SNTs more suitable for managing larger sums, such as inheritances or insurance payouts, rather than smaller, short-term savings.

Spending rules also differ significantly. Emergency funds can be used for virtually anything – groceries, rent, medical bills, or even car repairs. SNTs, however, are restricted to covering supplemental needs like therapy, assistive devices, or recreational activities. Using SNT funds for basic needs such as food or housing can reduce SSI benefits due to In-Kind Support and Maintenance rules, making it crucial to use these funds carefully.

When to Use an Emergency Fund

An emergency fund provides quick access to cash when unexpected expenses arise. If you’re not restricted by asset thresholds for benefits, this type of savings allows you to sidestep the complexities that come with setting up a special needs trust.

Speed is a key advantage of an emergency fund. Imagine your child’s communication device breaks down – you can replace it immediately without waiting for trustee approval. The same applies to essential medical equipment, uninsured therapy sessions, or sudden caregiver costs. With direct control over the funds, you can act quickly, avoiding delays that could disrupt daily life or critical care.

Emergency funds also offer flexibility for basic living expenses. Unlike Special Needs Trusts, which can reduce Supplemental Security Income (SSI) if used for housing or food, an emergency fund can cover essentials like rent, groceries, and utilities without penalties. This makes it a practical option for both everyday needs and unexpected autism-related costs.

For smaller amounts, an emergency fund is often the better choice. Setting up a Special Needs Trust involves attorney fees and ongoing trustee costs, which may not be worth it for modest sums. For example, if you receive a small inheritance under $14,000, putting it in an emergency fund or an ABLE account is more cost-effective. This approach avoids high setup and maintenance fees while still supporting your financial goals. These benefits highlight why an emergency fund can be a smart, practical solution in certain situations, especially when compared to special needs trusts.

When to Use a Special Needs Trust

A special needs trust becomes essential when your autistic child has or is expected to receive assets exceeding $2,000 – the limit for SSI and Medicaid eligibility. Even relatively modest inheritances, life insurance payouts, or settlement awards can unintentionally disqualify them from these critical benefits.

For larger inheritances or unexpected financial windfalls, a special needs trust ensures that funds are protected while maintaining eligibility for government assistance. Unlike ABLE accounts, which have annual contribution limits of around $18,000 to $19,000 and exclude only the first $100,000 from SSI resource testing, special needs trusts have no such restrictions. This makes them indispensable when other savings tools fall short.

Third-party special needs trusts are particularly useful for estate planning. They allow family members to set aside funds for the child without triggering Medicaid’s payback requirement upon the child’s passing.

A trustee – whether a family member, attorney, or corporate fiduciary – manages the trust to ensure that funds are used appropriately without jeopardizing the child’s benefits. The trust can cover expenses not typically funded by government programs, such as specialized therapy, adaptive technology, home accessibility modifications, and private caregiving services.

Setting up a special needs trust typically costs between $2,000 and $5,000, with annual trustee fees ranging from 1% to 2% of the trust’s assets. These costs, while significant, are a worthwhile investment in securing your child’s long-term care and financial stability.

Combining Emergency Funds with Special Needs Trusts

Using both an emergency fund and a special needs trust can provide a well-rounded financial plan for your autistic child. The emergency fund, often managed through an ABLE account, is ideal for handling day-to-day expenses and unexpected costs. Meanwhile, the special needs trust ensures long-term financial security and safeguards larger assets like inheritances or settlements. Together, these tools create a balance between immediate accessibility and future stability.

An ABLE account is perfect for covering immediate needs like medical co-pays, therapy sessions, or car repairs. On the other hand, a special needs trust is designed for more substantial costs, such as specialized autism therapies, home modifications, or adaptive technology, all without risking eligibility for public benefits.

For a seamless approach, consider this strategy: Use funds from the special needs trust by routing them through the ABLE account for certain expenses, like housing or groceries. If a trustee directly pays rent from the trust, it could lead to a reduction in Supplemental Security Income (SSI) due to In-Kind Support and Maintenance rules. However, transferring the money to the ABLE account first and then using it for these costs helps avoid that issue.

It’s essential to work closely with a special needs planning attorney to ensure all distributions align with Social Security Administration guidelines. This ensures compliance with the $100,000 SSI exclusion and the annual $19,000 contribution limits for ABLE accounts.

Conclusion

Emergency funds and special needs trusts serve distinct roles in financial planning. An emergency fund provides quick access to cash for family-wide crises, but it counts toward the $2,000 asset limit for government benefits like SSI. On the other hand, a special needs trust safeguards assets while ensuring your child’s long-term needs are met without affecting their benefit eligibility.

It’s important to know when to use each. For smaller sums needed for everyday expenses, an ABLE account can be a practical choice. For larger assets, such as inheritances or life insurance proceeds, a third-party special needs trust is a better option. This type of trust avoids Medicaid payback requirements and doesn’t have contribution limits.

Once immediate financial needs are covered, shift your focus to long-term planning. Start by separating short-term emergencies from long-term asset protection. Build an emergency fund to stabilize your family’s finances, then protect your child’s eligibility for benefits by leveraging tools like an ABLE account or a special needs trust. If you’re planning to leave an inheritance, consulting a special needs planning attorney is crucial. A third-party trust can prevent your child from losing access to essential government benefits due to receiving cash directly.

When considering long-term care, choosing the right trustee is critical. A trustee must understand the "In-Kind Support and Maintenance" rules to avoid SSI benefit reductions. While professional trustees bring financial expertise, family members may provide a more personal connection and commitment to your child’s well-being.

FAQs

How much should I keep in an emergency fund if my child gets SSI?

If your child receives SSI, it’s a good idea to have an emergency fund that can cover 3–6 months of essential costs, such as rent, utilities, and groceries. However, keep in mind SSI’s $2,000 resource limit to avoid jeopardizing eligibility. Managing your savings carefully allows you to handle surprises without putting your child’s benefits at risk. The amount you’ll need will depend on your family’s unique income and expenses.

What expenses can an SNT pay for without reducing SSI?

A Special Needs Trust (SNT) can pay for certain disability-related expenses without jeopardizing Supplemental Security Income (SSI) benefits. These expenses often include things like medical treatments, therapy sessions, educational programs, and specific personal needs tied to the individual’s disability or blindness. However, it’s crucial to note that payments for food or housing can affect SSI eligibility. Understanding the rules around SNT distributions is essential to avoid any unintended consequences.

Do I need an ABLE account if I already have an SNT?

While both ABLE accounts and Special Needs Trusts (SNTs) are designed to support individuals with disabilities, they work differently and often complement each other. ABLE accounts are tax-advantaged savings plans meant for everyday expenses and smaller purchases. On the other hand, SNTs can manage larger amounts of money without jeopardizing eligibility for SSI or Medicaid, covering broader or less frequent expenses. Many families choose to use both options together, combining short-term flexibility with long-term financial security.