Raising a child with autism can strain family finances, but planning can help manage costs and secure long-term stability. Families often face high therapy expenses, reduced household income, and challenges accessing benefits. Here’s a quick breakdown:

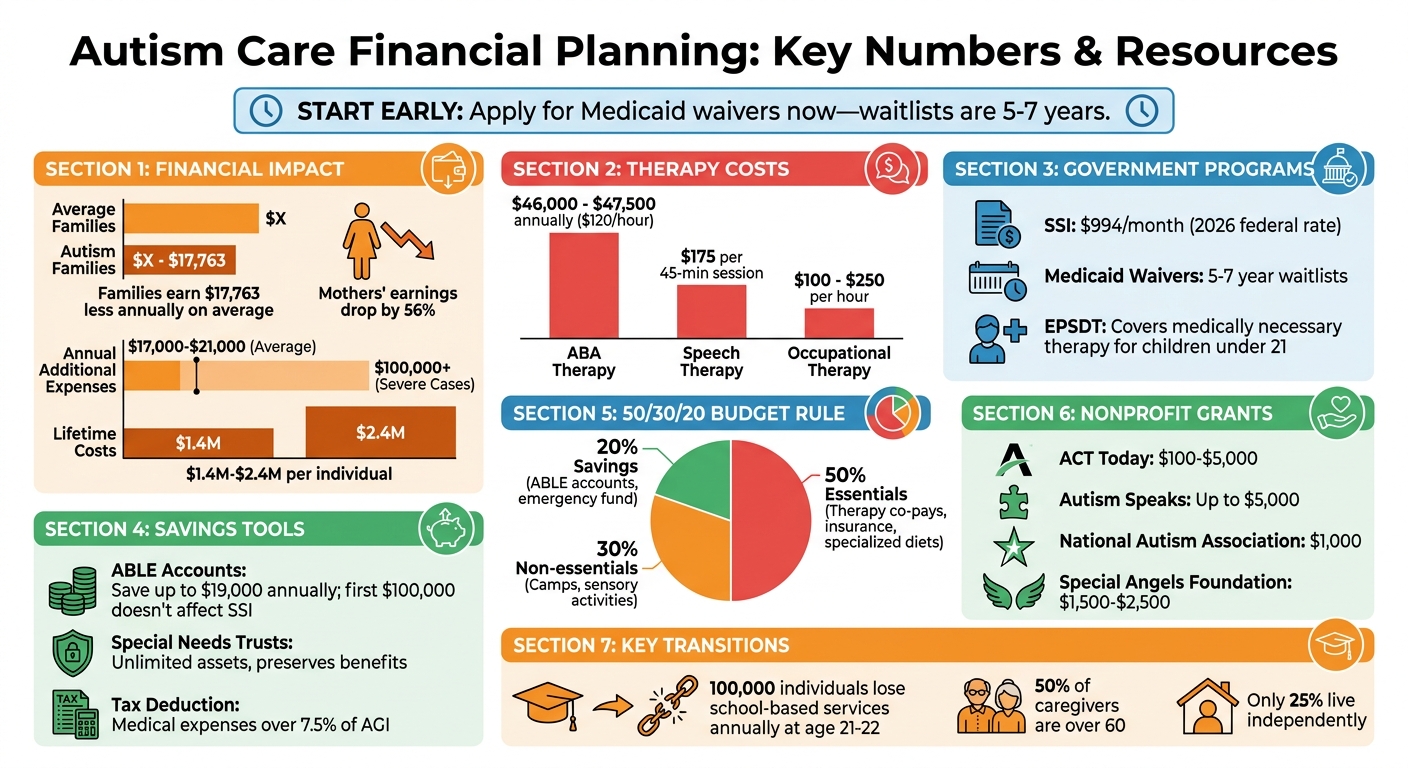

- Financial Impact: Families with autistic children earn $17,763 less annually on average. Mothers’ earnings drop by 56%.

- Therapy Costs: ABA therapy costs $46,000–$47,500 annually; speech/occupational therapy is $100–$250 per hour.

- Lifetime Costs: Supporting an autistic individual can total $1.4M–$2.4M.

- Key Tools: SSI ($994/month in 2026), Medicaid, ABLE accounts (save up to $100,000 without affecting SSI), and Special Needs Trusts.

- Budget Tip: Use the 50/30/20 rule – 50% for essentials, 30% for non-essentials, 20% for savings.

- Apply Early: Medicaid waivers often have 5–7 year waitlists.

Planning involves combining resources like insurance, government programs, and nonprofit grants. Tracking expenses and leveraging tools like ABLE accounts and Special Needs Trusts can protect benefits and ensure your child’s future. Start early, stay organized, and focus on both immediate and long-term needs.

Autism Care Financial Planning: Costs, Programs, and Savings Tools at a Glance

Estimating and Managing Autism Care Costs

Understanding Lifetime Costs of Autism Care

Planning for autism care begins with understanding how costs can vary based on individual needs. On average, families spend an additional $17,000 to $21,000 per year on autism-related expenses, though this amount can climb above $100,000 annually for more severe cases [4].

Costs often increase during key life transitions. For example, when children with autism reach 21 or 22 and age out of school-based services, families face a sudden loss of support. Each year, nearly 100,000 individuals with autism in the U.S. lose access to these services, leaving families to seek out adult care options that are often harder to access and more expensive [6]. This phase presents a dual challenge: managing immediate expenses while planning for long-term care. Statistics highlight the urgency – 50% of caregivers for individuals with autism are over 60, and only 25% of individuals with autism live independently [6].

Creating a Budget for Autism Care

Building a budget for autism care requires pulling together multiple funding sources, such as Regional Center funding, private insurance, Supplemental Security Income (SSI), and ABLE accounts [2]. It’s important to note that Regional Centers and state programs typically step in only after private insurance and school district funding have been used [2]. Keeping detailed records of expenses is essential for applying for these resources [2].

A helpful method for budgeting is the 50/30/20 rule:

- 50% for essentials: Therapy co-pays, medical premiums, specialized groceries, and home safety modifications.

- 30% for non-essentials: Sensory-friendly activities, specialized camps, and social skills classes.

- 20% for savings and debt repayment: Contributions to ABLE accounts, Special Needs Trusts, or an emergency fund [5].

"The hardest part of navigating autism funding is not filling out the applications. It is sitting at that kitchen table, looking at the numbers, and deciding to keep going anyway."

– Justin Bowman, Founder, VizyPlan [1]

This structured approach not only helps manage immediate needs but also sets the stage for accessing additional resources, as discussed in the next section.

Sample Monthly Budget Template

Here’s an example of how a household with a $5,000 monthly income might allocate their budget:

| Budget Category | Monthly Allocation | Autism-Specific Examples |

|---|---|---|

| Needs (50%) | $2,500 | Therapy co-pays (ABA, OT, Speech), medical insurance premiums, specialized diets, home safety modifications |

| Wants (30%) | $1,500 | Sensory-friendly movie screenings, specialized summer camps, social skills classes, weighted blankets |

| Savings/Debt (20%) | $1,000 | ABLE account contributions, Special Needs Trust funding, emergency fund for unexpected medical or equipment costs |

Additionally, unreimbursed medical expenses that exceed 7.5% of your Adjusted Gross Income (AGI) are tax-deductible [1][2]. For example, if your annual income is $60,000, any unreimbursed expenses over $4,500 could reduce your tax liability [1][2]. Keeping thorough records of therapy sessions, evaluations, and specialized equipment purchases can lead to substantial tax savings over time.

sbb-itb-d549f5b

Autism Speaks CEO Keith Wargo on Financial Planning for Families with Autism

Financial Assistance Programs and Resources

Having a clear budget is just one piece of the puzzle. Knowing what financial aid is available can make managing autism care much more manageable.

Government Support Programs

Both federal and state governments offer programs to help offset the costs of autism care. Supplemental Security Income (SSI) provides monthly payments to individuals with disabilities who meet income and resource limits. For 2026, the federal benefit rate is $994 per month for an individual [2]. Similarly, Social Security Disability Insurance (SSDI) supports adults who became disabled before age 22, using a parent’s Social Security earnings record [2].

Medicaid, known as Medi-Cal in California, is the largest source of funding for autism services in the U.S. Through Home and Community-Based Services (HCBS) waivers, states can pay for services like respite care, day programs, and supported employment [1][2]. However, due to high demand, waitlists can range from 5 to 7 years in many states, so early application is crucial [1]. For children under 21, Medicaid’s Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) program ensures coverage for any therapy deemed "medically necessary", even if it’s not part of the standard state plan [1].

In California, Regional Centers fund services outlined in an Individual Program Plan (IPP) but only after other funding sources – like private insurance or school districts – are exhausted.

"The regional center is the ‘payer of last resort.’ This means you must exhaust all other potential funding sources, such as private insurance or school district funding, before the regional center will pay." – Meristem [2]

Another California-specific option is In-Home Supportive Services (IHSS), which pays for in-home care providers, offering up to 283 hours of paid care per month [7]. Additionally, the Children’s Health Insurance Program (CHIP) provides health insurance for children under 19 in families that earn too much for Medicaid but can’t afford private insurance [7]. To speed up applications, gather detailed medical records, diagnosis reports, and proof of functional limitations in advance [7].

Nonprofit organizations can also provide critical financial support for families.

Nonprofit Grants and Scholarships

Nonprofits are a vital resource for covering costs like therapy, medical equipment, and safety devices. Families can apply to multiple organizations simultaneously [1]. Here are some examples:

- ACT Today: Offers grants between $100 and $5,000 for families earning less than $100,000 per year [1].

- Autism Speaks: Provides community grants of up to $5,000 for therapy, camp, or equipment [1].

- National Autism Association: Awards one-time $1,000 grants to families with incomes under $50,000 annually [1].

- The Flutie Foundation: Has allocated over $900,000 for assistive technology programs since 2012 [1].

- Special Angels Foundation: Grants between $1,500 and $2,500 for therapy and equipment [1].

- Ben’s Fund: Offers up to $1,000 annually for summer camps or enrichment classes [1].

- UnitedHealthcare Children’s Foundation: Covers medical expenses not fully paid by insurance, and you don’t need to be a UnitedHealthcare member to apply [1].

For students with autism pursuing higher education or vocational training, the Organization for Autism Research (OAR) offers scholarships [2]. Families can apply to multiple nonprofits at the same time to fill gaps left by insurance [1].

Insurance and Private Funding Options

All 50 states and Washington, D.C., require insurance plans to cover autism therapies like ABA [1]. However, self-funded plans governed by ERISA may be exempt. These plans must still comply with the federal Mental Health Parity and Addiction Equity Act, which ensures autism coverage is on par with physical health coverage [1]. To find out if your plan is self-funded or fully insured, ask your employer [1].

Some states limit autism coverage. For instance, Florida caps ABA therapy at $36,000 annually, with a $200,000 lifetime maximum [1]. To avoid surprises, review your insurance policy carefully, paying attention to age limits, annual caps, and prior authorization requirements for therapies like ABA, speech, and occupational therapy [1].

Families can also reduce costs by combining funding sources. For example, private insurance can cover therapy, SSI can handle living expenses, and ABLE accounts can fund recreation or specialized equipment [2].

ABLE accounts provide tax-advantaged savings for disability-related expenses without affecting eligibility for programs like SSI or Medicaid. Starting in 2026, eligibility will expand to include individuals whose disability began before age 46 (up from age 26), making the program accessible to millions more Americans [1].

For families juggling multiple funding streams, consulting a Chartered Special Needs Consultant (ChSNC®) can help create a long-term financial plan. These professionals can integrate savings, life insurance, and special needs trusts into a cohesive strategy [2]. Combining these resources can provide both immediate relief and long-term security.

Planning for Long-Term Financial Security

Once you’ve addressed immediate financial needs, it’s time to think about the bigger picture. This means creating a safety net that not only protects your child’s future but also ensures your own financial well-being.

Special Needs Trusts and ABLE Accounts

A Special Needs Trust (SNT) is a legal tool designed to hold assets for your child without affecting their eligibility for essential benefits like SSI or Medicaid. The assets are managed by a trustee and can be used for a variety of expenses that enhance your child’s quality of life, such as specialized therapies, electronics, or even travel [2].

"The assets in the trust are managed by a trustee and can be used to pay for a wide variety of expenses that are not covered by government benefits." – Meristem [2]

SNTs can hold unlimited assets, making them ideal for larger inheritances or payouts from life insurance policies [2]. However, setting one up requires the help of a special needs attorney, which can be costly. It’s also important to ensure that relatives, like grandparents, direct any inheritance or gifts into the SNT instead of leaving them directly to your child. This prevents the risk of disqualifying them from benefits [2].

On the other hand, ABLE accounts are a great complement to SNTs. These accounts are perfect for managing smaller, everyday expenses. In 2026, you can contribute up to $19,000 annually, and the first $100,000 saved doesn’t count toward SSI asset limits [1][2]. The funds grow tax-free and can be withdrawn without federal income tax, as long as they’re used for qualified disability expenses like housing, healthcare, or assistive technology [2][3].

"If your child receives SSI or Medicaid, an ABLE account lets you save for their future without jeopardizing the benefits they depend on today." – Justin Bowman, Founder of VizyPlan [1]

The key is to use both tools together: the ABLE account for frequent, smaller costs and the SNT for larger, long-term assets. This layered approach ensures your child’s needs are met now and in the future while simplifying financial planning as they grow.

Financial Planning for the Transition to Adulthood

As your child approaches adulthood, their financial and medical needs may change. Planning ahead can help you navigate this transition smoothly. For instance, when your child turns 18, you may need to establish guardianship or conservatorship to continue making decisions on their behalf. Alternatively, less restrictive options like supported decision-making might be more appropriate [2].

Funding this transition often requires multiple sources. Combining SSI or SSDI (offering $994 per month in 2026 [2]), Medicaid Home and Community-Based Services (HCBS) waivers, and personal savings through ABLE accounts can help cover essential expenses. In California, Regional Centers can also provide funding for services outlined in an Individual Program Plan (IPP), though private insurance and school district resources are used first [2].

| Service/Need | Primary Funding Source | Secondary/Supplemental Source |

|---|---|---|

| Transition Program Tuition | Regional Center / State Grants | Family Resources |

| Therapy & Medical Care | Private Insurance / Medicaid | Medicaid Waivers |

| Housing & Food | SSI / SSDI | ABLE Account |

| Employment Support | HCBS Waivers / Vocational Rehab | Student Earned Income Exclusion |

| Quality of Life/Recreation | ABLE Account | Special Needs Trust / Scholarships |

Because HCBS waivers often have long waitlists, it’s wise to apply as early as possible [2]. Keeping thorough records of medical bills, therapy reports, and educational assessments can also strengthen applications for benefits [2]. To simplify this complex process, consider working with a Chartered Special Needs Consultant (ChSNC®) or a special needs attorney who can help coordinate funding streams and ensure compliance with all rules [2][3].

Protecting Your Own Financial Future

Caring for a child with autism can strain a family’s finances. Studies show that families of children with autism earn an average of $17,763 less per year compared to families without health limitations [1]. Balancing caregiving responsibilities with your own financial security is critical.

Start by building an emergency fund with three to six months of living expenses in an easily accessible account [3]. This fund can help cover unexpected disruptions in care or income. At the same time, prioritize your retirement savings. Draining your 401(k) or IRA to pay for current expenses could leave you without sufficient funds for your own future or your child’s long-term needs.

Life insurance is another important consideration. Policies that fund a Special Needs Trust after your death can ensure your child has financial support even when you’re no longer around [2]. A ChSNC® can help integrate life insurance, savings, and trusts into a cohesive plan tailored to your family’s unique situation [2]. By securing your own financial future, you’re also ensuring your child’s long-term stability.

Using Technology to Track and Manage Expenses

Managing the variety of costs associated with autism care can feel daunting. Families often allocate about 10% of their net income to out-of-pocket autism-related expenses [8]. Without a clear system to monitor spending, it becomes tough to spot patterns, focus on the most impactful interventions, or maintain the detailed records needed for government benefits and insurance appeals. Using technology to streamline these processes is a practical way to create a manageable caregiving budget, as discussed earlier. A digital system for tracking expenses can make navigating these costs much more efficient.

Tracking Autism-Related Expenses with Guiding Growth

Guiding Growth simplifies expense tracking by consolidating all autism-related costs into one platform. Its event logging tools allow families to monitor both direct expenses – like ABA therapy, which costs around $120 per hour [10], and speech therapy, averaging $175 per 45-minute session [1] – and indirect expenses such as transportation (deductible at 21 cents per mile for tax purposes [1]) and lost income due to time off work.

"Keep detailed records of all of your child’s expenses, including medical bills, therapy reports, and educational assessments. This will be helpful when applying for benefits and services." – Meristem [2]

By logging these expenses, families can build a digital record that plays a crucial role in securing Regional Center funding, maintaining SSI/Medicaid eligibility, and claiming tax deductions for unreimbursed expenses exceeding 7.5% of adjusted gross income (AGI) [2][9]. Guiding Growth also helps identify recurring costs and potential savings, such as switching providers or reallocating funds. Once your expenses are recorded, combining this data with behavioral insights can further enhance your financial decision-making.

Connecting Behavioral Data to Financial Decisions

One standout feature of Guiding Growth is its ability to link behavioral and health data with financial records. By tracking therapy sessions, dietary changes, and behavioral events in one system, families can evaluate which interventions truly benefit their child’s development. This allows you to focus your spending on services that deliver meaningful results [9], rather than continuing with therapies that may not be effective.

For instance, if you’re investing $50,000 or more annually in intensive behavioral interventions [8], it’s crucial to determine whether this expense is improving your child’s regulation, communication, or daily life skills. Reviewing behavioral trends alongside expense data can guide smarter spending decisions. This is especially important since families with autistic children typically earn an average of $17,763 less per year [1], making it essential to allocate resources wisely. Consistent tracking also ensures your spending stays aligned with your budget, enabling you to adapt quickly to new or changing costs [9].

Conclusion and Key Takeaways

Navigating the financial demands of autism care requires consistent planning and adaptability. It’s not a one-and-done process but an ongoing effort to piece together a support system that meets your family’s needs. One key reality? No single funding source will cover everything. Instead, families often rely on a mix of resources to create a sustainable plan. Combining funding streams, while enrolling early on waitlists that can take 5 to 7 years, lays the groundwork for long-term stability.

Start with the basics: apply for Medicaid and SSI to access additional services, maximize school-based IEP supports, and consider opening an ABLE account, which allows you to save up to $20,000 annually without jeopardizing benefits. Maintaining organized records – such as medical bills, therapy notes, and educational assessments – is equally important. Not only will these documents help when applying for benefits or claiming tax deductions (for medical expenses exceeding 7.5% of your adjusted gross income), but they’ll also ensure you’re prepared to advocate for your child’s needs effectively.

Technology can simplify these complexities. Tools like Guiding Growth centralize expense tracking while integrating behavioral and health data, helping families make informed decisions about interventions. For those investing $40,000–$60,000 annually in intensive therapies [11], understanding what truly works isn’t just helpful – it’s critical.

"The hardest part of navigating autism funding is not filling out the applications. It is sitting at that kitchen table, looking at the numbers, and deciding to keep going anyway." [1]

FAQs

What should I do first if I’m overwhelmed by autism-related costs?

If the costs associated with autism feel daunting, consider looking into financial assistance programs such as Medicaid, Waivers, and Supplemental Security Income (SSI). Additionally, various state or federal programs may offer support. Another helpful tool is an ABLE Account, which allows you to save for long-term needs without jeopardizing eligibility for public benefits. Taking the time to research these options can help you understand eligibility requirements and create a practical plan for managing expenses.

How can I save money for my child without losing SSI or Medicaid?

To set aside money for your child without risking their SSI or Medicaid benefits, ABLE Accounts are a great option. These are specially designed, tax-advantaged savings accounts for individuals with disabilities. Additionally, programs like Medicaid Waivers and SSI at both federal and state levels can provide valuable support. For more tailored strategies, it’s wise to work with professionals experienced in special needs planning. They can help you set up trusts or other financial tools to ensure your child’s benefits remain intact while managing savings effectively.

How early should I apply for Medicaid waivers and other benefits?

Applying for Medicaid waivers and similar benefits early is crucial to avoid unnecessary delays. Many of these programs come with specific eligibility criteria and waiting lists, so starting the process sooner increases your chances of accessing resources when you need them. To get started, reach out to your local County Office of Mental Health and Intellectual Disabilities (MH/ID) or the Office of Developmental Programs (ODP). They can guide you through the steps and help secure the support you’re looking for.